Don't Try To Catch A Falling "Naira"

Godwin Emefiele finds a new scapegoat for Naira weakness

Last week I had a conversation in a Whatsapp group about Nigeria’s dire economic conditions. There were some disagreements on the question of whether Nigeria has a debt problem, but the consensus was that Nigeria has a currency problem, driven by deep ingrained structural economic problems. Which also led to the latest blunder by central governor Godwin Emefiele. Last week he blamed the owner of abokifx.com for manipulating exchange rates for personal gains, using various business bank accounts. How much truth there is in this claim will come to light in due time, the site has since stopped providing quotes. Truthfully, the whole thing seems like a deflection to me.

At first it seems that relative to other oil exporters, Nigeria had never learnt to manage its oil revenues properly. When the going was good and oil prices rose, they would increase spending on non-economically viable expenditure. When things were bad and reserves were not adequate, they would resort to punitive import restrictions and other clever tactics to ration USD outflows, mostly leading to high inflation locally and driving up debt servicing costs.

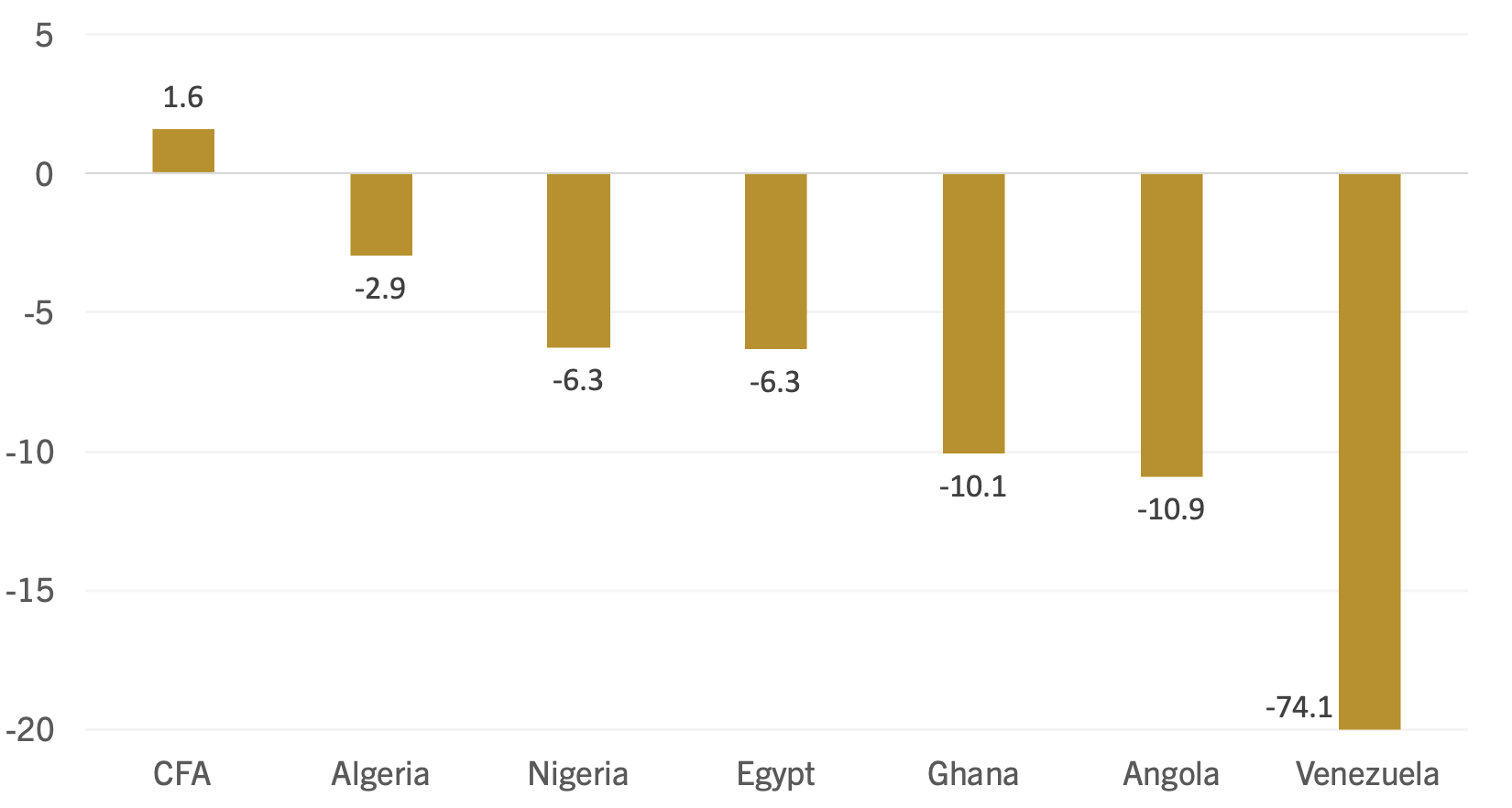

However, over the last 20 years, the Naira has lost about 6.3% of its value every year. Which to my surprise is on par with the Egyptian pound and not too far from the Algerian dinar (both countries arguable in better shape economically).

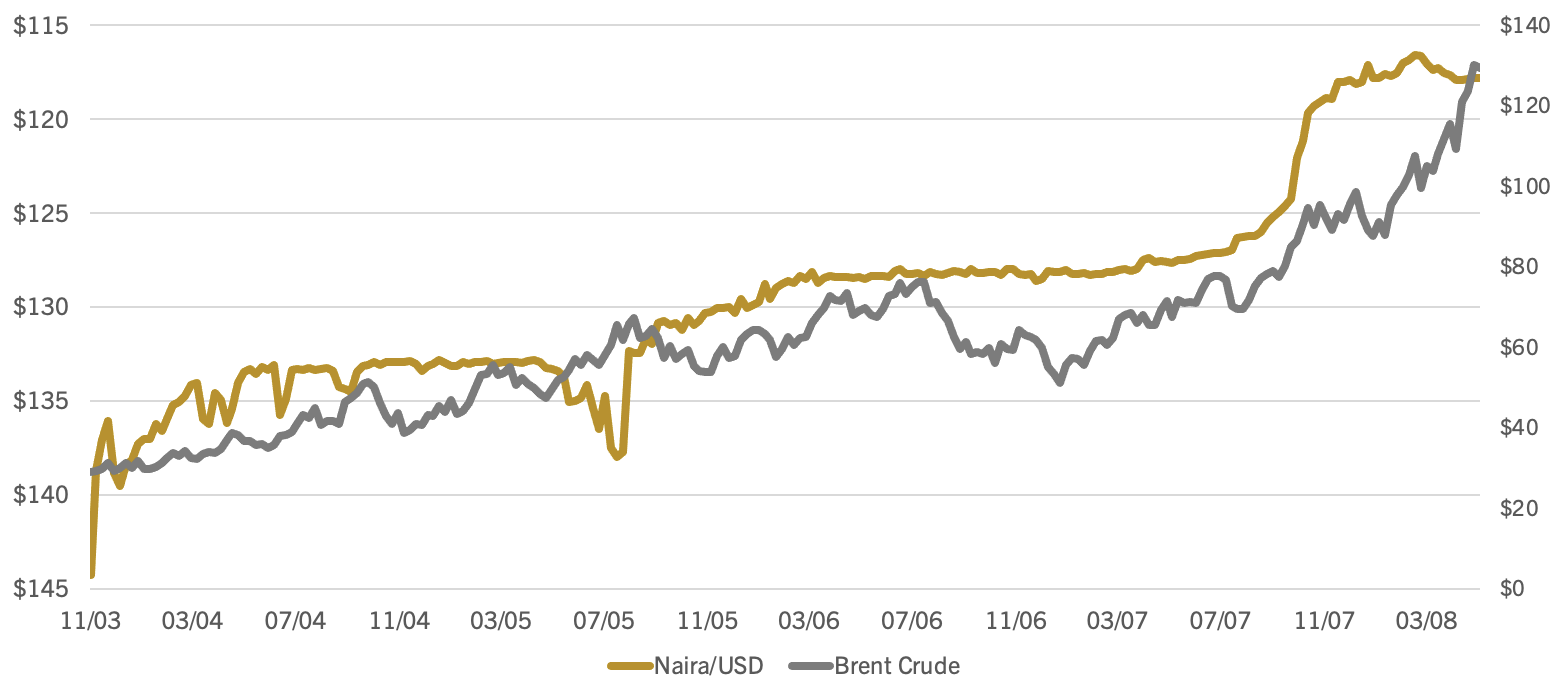

Below is a chart of the official Naira/USD exchange rate since 1993, the travel of direction is clear and consistent, except for a few odd periods. The period spanning between late 2003 to mid 2008 (circled below) stands out, as the Naira strengthened by more than 20% against the USD without any intervention by the authorities. Notably the longest period of appreciation Naira over the period.

Oil prices started to rise steadily in late 2003 from around $30 per barrel till they peaked at $140 per barrel in 2008, further Nigeria received $18bn debt relief from the Paris Club (happy days). The high oil prices allowed Nigeria’s foreign exchange reserves to rise drastically, and the Excess Crude Account rose 4x to $20bn (by 2018, that number was closer to $1.8bn). These developments occurred under the rule of central bank governor Chukwuma Soludo. For the first time Nigeria had more USD than it needed, the black market exchange rate converged close to the official exchange rate, and people could obtain USD to import many more items than before.

When the bubble did burst in 2008, and oil prices fell, Nigeria was in a strong position to weather the storm. Foreign reserves stood at $62bn (compared to $35bn today). Nonetheless, Soludo banned the interbank market trading for 6 months, and devalued the Naira. About 12 months later oil prices started to recover, but Nigeria’s foreign exchange reserves did not. At the time there was also 12 month minimum holding period that foreign investors had to adhere to when buying Nigerian government bonds, which was the main impediment to Nigeria being included in the JP Morgan Bond Index (a benchmark that most bond investors follow). Consequently, this restriction was removed, and USD started pouring in to buy high yielding government bonds. The only issue was the money left as swiftly as it came in, as foreign investors repatriated most of their USD back to their home countries within a few months of holding the bonds.

The IMF and World Bank believe at least part of the solution is to aggressively devalue the Naira, which the central bank has done on many occasions but never with long lasting success. The rational is often that, this will boost exports and entice foreigners to import more, which in turn means more demand for the Naira. However Nigeria does not produce much locally (trade balance is positive mainly due to crude oil exports), and despite having relatively low government debts in USD (roughly $35bn or 8-10% of GDP), more than 50% of government revenues are spent on paying back interest and principal on these debts. A weaker Naira makes debt service payments higher, and imports more expensive for business, so the devaluation argument may not be as sound as the Econ. textbooks may tell us.

The obvious structural changes that need to be made are no different to those in many other developing countries. Nigeria needs more buyers of products priced in Naira, a more diversified export base and more value-add products not just raw materials. Then there is the more complex political influence on monetary policy which drives much of the currency market interventions.

As of writing the official exchange rate is at NGN411 to $1. On the black-market, the rate is round 30% more at NGN530 to $1.

Have a good weekend all.

Nice work - I believe the 20% appreciation from 03-07 is in part due to USD inflows looking to buy equity in Nigeria, among other things. at that time there was a boom in EM/FM investing. The stocks peaked before the GFC and have never recovered to those levels. I wonder if that trend is observable in the Egyptian Pound and other popular EM/FM investing locations in that period.